Futures Market: Overnight, LME copper opened at $9,754.5/mt. It held up well initially, reaching a high of $9,785.0/mt during the volatile session, before declining steadily to a low of $9,720.5/mt. It eventually closed at $9,725.0/mt, down 0.45%. Trading volume was 13,107 lots, and open interest was 286,326 lots. The overall trend was volatile initially, followed by a downward trend. The SHFE copper 2507 contract opened at 79,150 yuan/mt overnight, reaching a high of 79,290 yuan/mt during the session and a low of 79,030 yuan/mt at the end of the session. It eventually closed at 79,030 yuan/mt, down 0.13%. Trading volume was 21,972 lots, and open interest was 207,858 lots. The overall trend was an initial rally followed by a volatile decline.

[SMM Copper Morning Meeting Summary] News: (1) According to Morgan Stanley's latest global EV market data for April, global BEV sales in April 2025 increased 38% YoY to 1.0797 million units, with the Chinese market contributing over 60% of sales and a YoY growth rate of 51%.

(2) Container shipping activities from China to the US increased gradually in early June, leading investors to anticipate a potential second wave of early stockpiling to avoid tariffs before the peak summer shipping season. This could provide reasons for optimism in the stock market. Additionally, data showed that ocean freight rates for containers shipped from China and East Asia to the US West Coast surged 94% in the latest week.

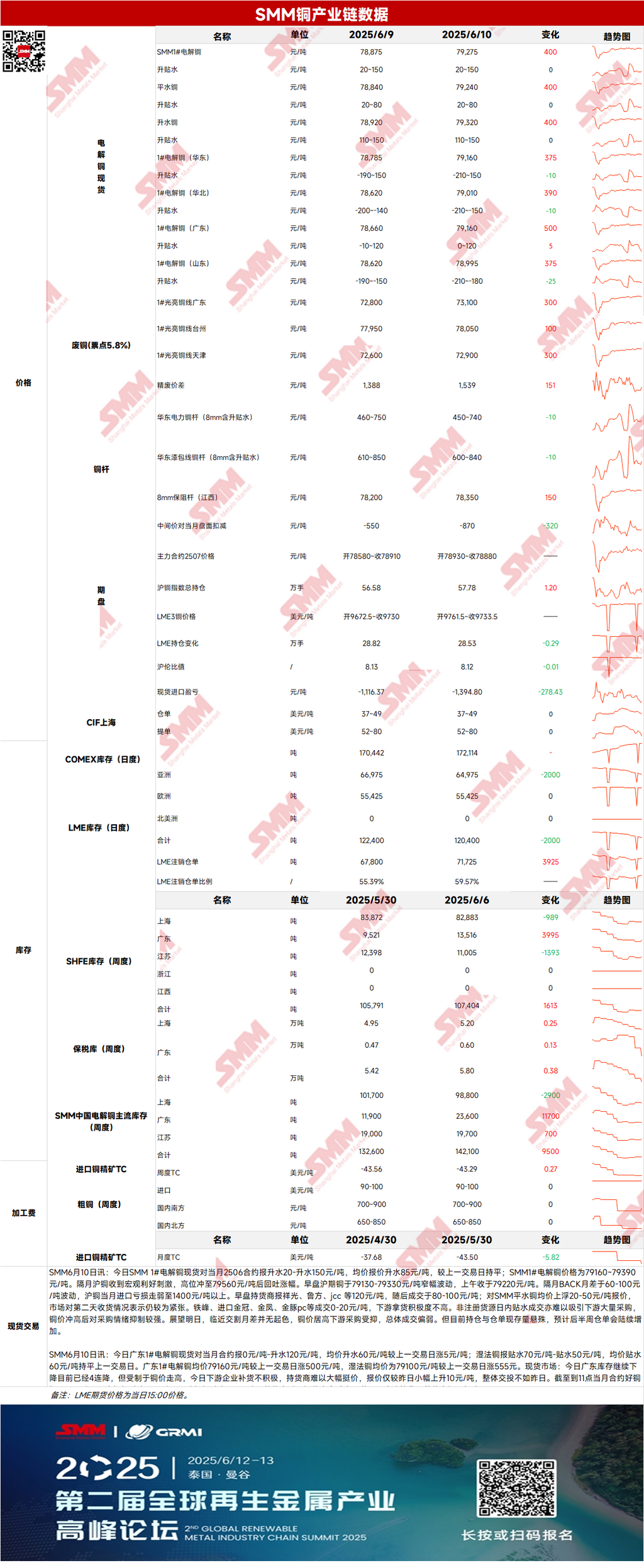

Spot: (1) Shanghai: On June 10, SMM #1 copper cathode spot prices were quoted at a premium of 20-150 yuan/mt against the front-month 2506 contract, with an average premium of 85 yuan/mt, unchanged MoM. With the approaching delivery month showing no improvement in the price spread and high copper prices suppressing downstream purchases, overall trading was weak. However, given the significant difference between current open interest and warrant inventory, warrants are expected to increase gradually in the latter half of the week.

(2) Guangdong: On June 10, Guangdong #1 copper cathode spot prices were quoted at 0-120 yuan/mt premium against the front-month contract, with an average premium of 60 yuan/mt, up 5 yuan/mt MoM. Overall, with copper prices rising and downstream buyers reluctant to rush to buy amid continuous price rise, overall trading was weaker than the previous day.

(3) Imported copper: On June 10, warrant prices ranged from $37 to $49/mt, with a QP of June, and the average price was unchanged MoM. B/L prices ranged from $52 to $80/mt, with a QP of July, and the average price was unchanged MoM. EQ copper (CIF B/L) prices ranged from $10 to $20/mt, with a QP of July, and the average price was unchanged MoM. Quotations were based on cargoes expected to arrive in mid-to-late June. Overall, tentative inquiries and offers increased, but buying and selling premiums remained fragmented.

(4) Secondary copper: On June 10, secondary copper raw material prices increased 300 yuan/mt MoM. Guangdong bare bright copper prices ranged from 73,000 to 73,200 yuan/mt, up 300 yuan/mt from the previous trading day. The price difference between copper cathode and copper scrap was 1,539 yuan/mt, continuing to increase by 151 yuan/mt MoM. The price difference between copper cathode rod and secondary copper rod is 1,465 yuan/mt. According to the SMM survey, the center of copper prices continues to move higher, with some suppliers of secondary copper raw materials starting to increase their shipments, believing that market sentiment is gradually improving during the US-China trade negotiations. If the outcome of the US-China trade talks falls short of expectations after their conclusion, copper prices may experience a significant pull back, leading to unnecessary losses. Therefore, suppliers of secondary copper raw materials have been selling at highs over the past two days.

(5) Inventory: On June 10, LME copper cathode inventories decreased by 2,000 mt to 120,400 mt; on the same day, SHFE warrant inventories fell by 496 mt to 33,746 mt.

Price: On the macro front, US and China economic and trade officials continued their second day of consultations in London, UK, on June 10. US Commerce Secretary Raimondo reportedly stated on the 10th that the negotiations were "progressing smoothly." According to informed sources, during this round of consultations, the US side is considering lifting a series of recently imposed restrictions involving areas such as chip design software, jet engine parts, ethane, and nuclear materials. Most of these measures were introduced in the past few weeks amid renewed tensions in US-China relations, with the condition that China relaxes restrictions on rare earth exports. Additionally, it is understood that India and the US are expected to reach a provisional trade agreement before month-end, and the US and Mexico are close to reaching an agreement on steel import tariffs. Amid uncertainties in trade prospects, market sentiment remains cautious, and copper prices closed slightly lower. On the fundamental front, high copper prices have dampened downstream procurement sentiment, with market trading activity remaining relatively weak. Overall, with the announcement of the US-China talks yet to be released, copper prices are expected to fluctuate at highs before the announcement.

》Click to view SMM Metal Database

[The above information is based on market collection and comprehensive assessment by the SMM research team. The information provided in this article is for reference only. This article does not constitute direct advice for investment research decisions. Clients should make cautious decisions and should not rely on this as a substitute for independent judgment. Any decisions made by clients are unrelated to SMM.]